Indian culture of destiny acceptance was always frowned upon by me as an act of lethargy camouflage. I had to roll back my thoughts after an event which thrust me in the forefront due to acts other than my own. A politician died. A girl posted remarks on the social network. She was arrested by the police. A magistrate exposed the charges as wrong. A student challenged Section 66A of the Information Technology Act.(hereinafter known as IT Act) This was all in the year 2012. Now here is where I come in for something I did in December 2000. I had written a book entitled ‘Guide to Information Technology Act 2000. It was sold out in two months to professionals as well as students.

‘Since I have used your book very often to lecture my fellow advocates, I thought of you’ said one Magistrate over the phone. The half hour conversation was summarized in my head that there were so many cases filed under the IT Act would need 27 years to clear assuming no more are filed in future. Suddenly a

statute relegated to student’s curriculum and library only became a front runner. They expected me to provide them a ‘fast-track’ solution for this since I was the only author-consultant combination in the field of Information Technology! This is when I contemplated my view on Destiny. Did I suddenly become the Hero

problem solver or a grass eating scapegoat?

I told the Magistrate ‘I need to know just one point, how did the cases under this statute pile up? I expected perhaps two low profile cases for every high profile one and at this rate from the year 2000 there should have been not more than a dozen.’ The man on the other end of the line laughed ‘All cases are under this statute only.’ I was dumbfounded. He promised to email me the list of cases ‘on the Board’ of that day with some additional details to permit me to understand the situation.

Note from author: The following cases are purposely ridiculous to show how provisions of a statute can be twisted. Though the case may be thrown out, it causes distress to the charged persons. The cases could have been better made under other statutes.

The following list was emailed to me. Names of the parties are hidden.

Case under: section 43 a of the IT Act.

Case of: Multinational Company vs. Software application provider

Section in brief: Unauthorised Access.

Case in brief: A junior in the payroll section did not have access to Top management files but he could view them and when Union negotiations came to table, he tabled some embarrassing findings such as ‘entertainment allowances’ paid to some attractive persons working under the top management. Since the accidental access was granted by a bug in the software, the company who coded the software was sued.

Case under: section 43 b of the IT Act.

Case of: A Company vs. Hardware server (Computer server)

Section in brief: Downloading data without permission

Case in brief: Disaster recovery centre was to be opened by a VIP. Upon his pressing of a button the data from other city miles away was to be backed up. However nothing happened after he pressed the proverbial button. After a cursory glance it was reported that since the server had already backed up the data it would not do it again. Since no permission was granted to the server to download data before the VIP had opened the facility, the hardware (server) was sued. The server machine (!) was not re-presented by a Lawyer so the court had to provide one – after all, rules of the court need to be followed.

Case under: section 43 c of the IT Act.

Case of: Shopping Mall vs. Customers with cold (Names of the parties are hidden)

Section in brief: Introduces virus

Case in brief: A customer with severe and infectious cold went shopping in a mall. As he handed over cash he also handed over his virus. Many cashiers manning the computers, immediately fell sick. Since computer users were affected by the customer induced virus, they could not use the allocated computer to perform their allotted duty. Hence the customer was arrested.

Case under: section 43 d of the IT Act.

Case of: Retail Shop vs. Unidentified rioters (Names of the parties are hidden)

Section in brief: Damages, computer, software or data

Case in brief: Riots had broken out and before the party could down its shutters, a stone crashed through the display window and hit the computer which had stock and sales data. Since the computer repair person said it would take two days to repair the computer, the shop was forced to close down as stock and rates were all bar coded. (Other Indian Penal Code or Criminal provision was not used) As all the elements mentioned in the section were damaged, viz. computer, software and data, the company felt this was the most appropriate section to charge under!

Case under: section 43 e of the IT Act

Case of: A large company vs. Local electrician

Section in brief: disrupts or causes disruption of any computer, computer system or computer network

Case in brief: In a newly constructed building, a company was one of the few early occupants. In one office, some electrical work was in progress and the electrician started a machine needing high voltage. It tripped the electricity in the entire building. Since the work of this company was ‘disrupted’, they made a case against the electrician!

Case under: section 43 f of the IT Act

Case of: Employee of a company vs. Security guard of that same company

Section in brief: denies or causes the denial of access to any person authorized to access any computer system or computer network by any means

Case in brief: As per the instructions to the security, the guard stopped an employee without Identity card. Since he was a computer user who lost one day leave/salary, he sued the guard for preventing him from using his computer! (he was posted in the mail room and not any important position)

Additional case u/s 43f

Case under: section 43 f of the IT Act

Case of: A company vs. State Electricity Board

Section in brief: denies or causes the denial of access to any person authorized to access any computer system or computer network by any means

Case in brief: Though it was usual to accept power outages periodically other than on pre-determined day of the week in most parts of India, a company which got fed up with the lack of service, decided to sue the Board on the grounds that their employees were denied access to their computer since there was no power and only the State Electricity Board was responsible for denial of power and eventually, denial of access to the computer!

Case under: section 43 g of the IT Act

Case of: Govt. vs. Network service provider

Section in brief: provides any assistance to any person to facilitate access to a computer in contravention of the provisions of the IT Act

Case in brief: A network service provider followed all KYC rules before connecting a subscriber who then hacked into various Government Websites. Even before he was charged, the service provider was charged because without the assistance of the network service provider, the hacker would not have had internet access in the first place!

I reported to the magistrate that during the passage of this Act, 5 other Acts were simultaneous amended which started a trend. The emphasis is on the word amendment which is not ‘replacement’. The cases show that the accusers have ‘replaced’ other Acts by IT Act.

Now don’t you feel that sections other than section 66A need review?

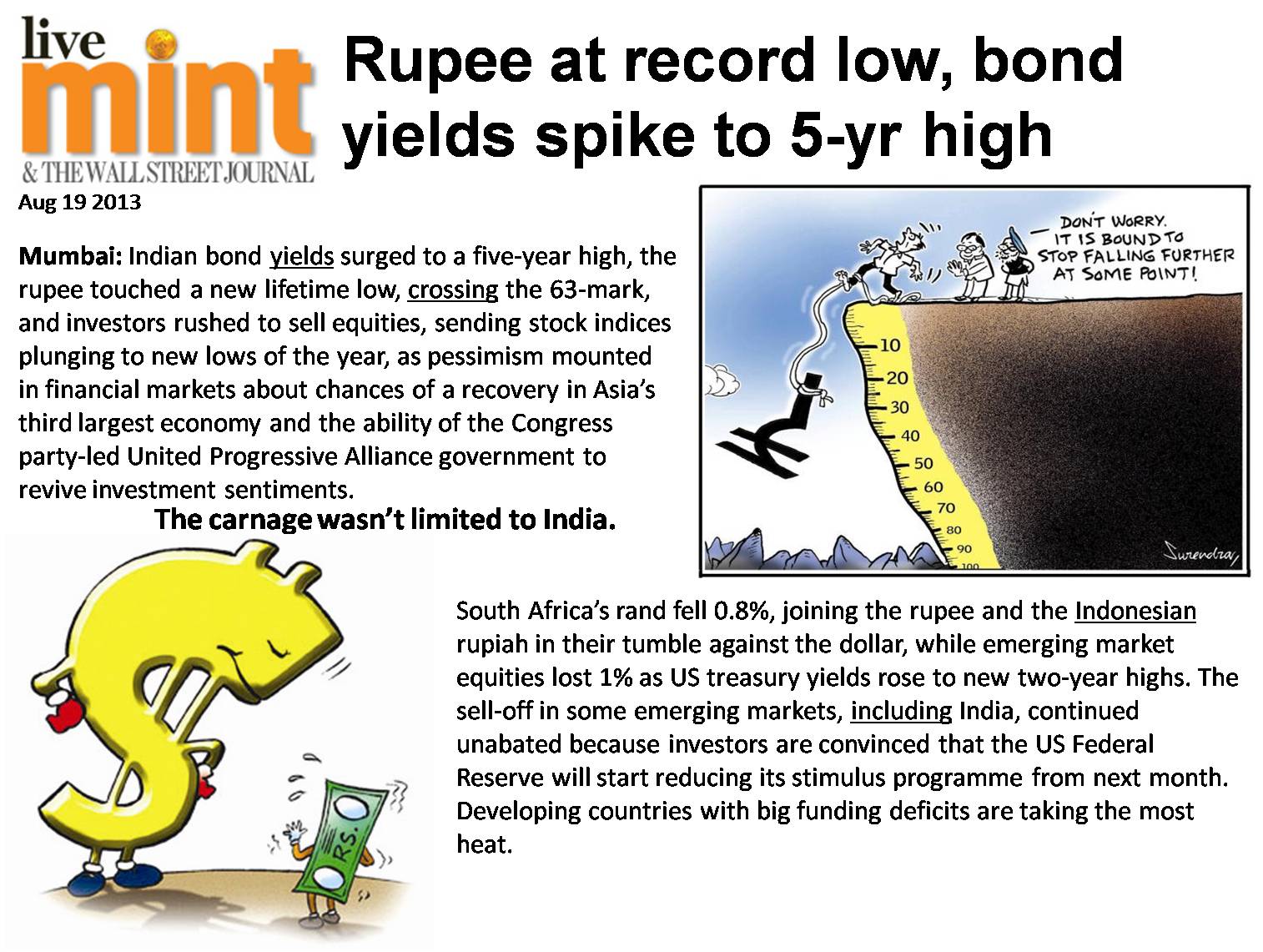

BELOW THE BELT: This is a foul in Boxing. But this is the impact on all of us as the food gets costlier and our stomachs are hit by the inflation which is the direct impact of fall in value of Rupee.

BELOW THE BELT: This is a foul in Boxing. But this is the impact on all of us as the food gets costlier and our stomachs are hit by the inflation which is the direct impact of fall in value of Rupee.

Dropped cylinder: This is a term from Drag Racing when a cylinder runs too rich (too much fuel in the air/fuel mixture) and prevents the spark plug(s) from firing.

Dropped cylinder: This is a term from Drag Racing when a cylinder runs too rich (too much fuel in the air/fuel mixture) and prevents the spark plug(s) from firing.

![BES’s Institute of Management Studies and Research [besimsr]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_uTpXHk3UTLixLOq5GePXgPPzXOrLOouZRHVrJeQuXXsjTHCBWFv-HuaNrAz1UNokxEucFnEadILh1qkTf6B3MlxA0dfqq7caivUZostvjAqICAbINHHePl2I64kmmQVcdnr2ztFgnx3i0mfSxG-gDCA_WMgLCPcsQUSjGDR3-hDlou48wauUS56iUqLq9x6wRpLYnR72RCMgAROhW7wg=s0-d)

{kind=link}